Buying a mobile home can be a smart, budget-friendly way to own a place of your own. But figuring out how to finance one? That’s where it gets tricky. Not every lender offers loans for manufactured homes, and not every mobile home qualifies for the kind of loan that actually makes things affordable.

If you’ve been looking into FHA loans and wondering whether they can help; good news: they can. In fact, they’re one of the most accessible options out there, especially if you don’t have perfect credit or a huge down payment saved up.

This guide walks you through everything you need to know, step by step from the types of FHA loans that apply to mobile homes, to what makes a property eligible, and how to improve your chances of getting approved.

FHA Programs for Mobile Homes

1. FHA Title I Loan: For Mobile Homes With or Without Land

Title I loans are made just for mobile or manufactured homes, even if you don’t own the land. This program lets you:

-

Finance just the mobile home

-

Finance the land it sits on

-

Or finance both together

The home can be placed in a mobile home park (as long as the lease meets FHA requirements), or on land you own or plan to buy. These loans typically come with shorter terms, up to 20 years for the home itself, and may have stricter limits on how much you can borrow. But they’re a solid option if you’re not buying land or if you’re placing your home in a community.

2. FHA Title II Loan: For Mobile Homes Permanently Installed on Owned Land

If you already own land, or plan to buy land along with your mobile home, Title II might be a better fit. This is the standard FHA loan most people know. It’s available for mobile homes only if the home is permanently attached to the land (think: real foundation, utilities connected, taxed as real estate).

You’ll need to meet a few extra requirements (more on that later), but in exchange, you’ll get a longer loan term, up to 30 years, and possibly lower interest rates. Plus, the loan limits are generally higher compared to Title I.

FHA Loan Comparison: Title I vs Title II for Mobile Homes

|

Feature |

FHA Title I |

FHA Title II |

|

What it covers |

Mobile home, lot, or both |

Mobile home + land (together as real estate) |

|

Land ownership required? |

No (leased land allowed) |

Yes (you must own the land) |

|

Permanent foundation required? |

No |

Yes |

|

Home classification |

Personal property |

Real property (must be legally classified as real estate) |

|

Loan term |

Up to 20 years (home), 15 years (lot), or 25 years (home + lot) |

Up to 30 years |

|

Loan amount limits |

Lower (e.g., ~$92K–$148K for home + lot) |

Higher (based on local FHA loan limits, up to ~$472K–$1M+) |

|

Credit & down payment |

Flexible, but varies by lender |

Minimum 3.5% down (580+ credit score) |

|

Mortgage insurance |

Required |

Required |

|

Where it's used |

Mobile home parks or private land |

Private land you own or are buying |

|

Eligible home type |

Manufactured home built after June 15, 1976 and HUD-certified |

Same as Title I, but must be permanently affixed |

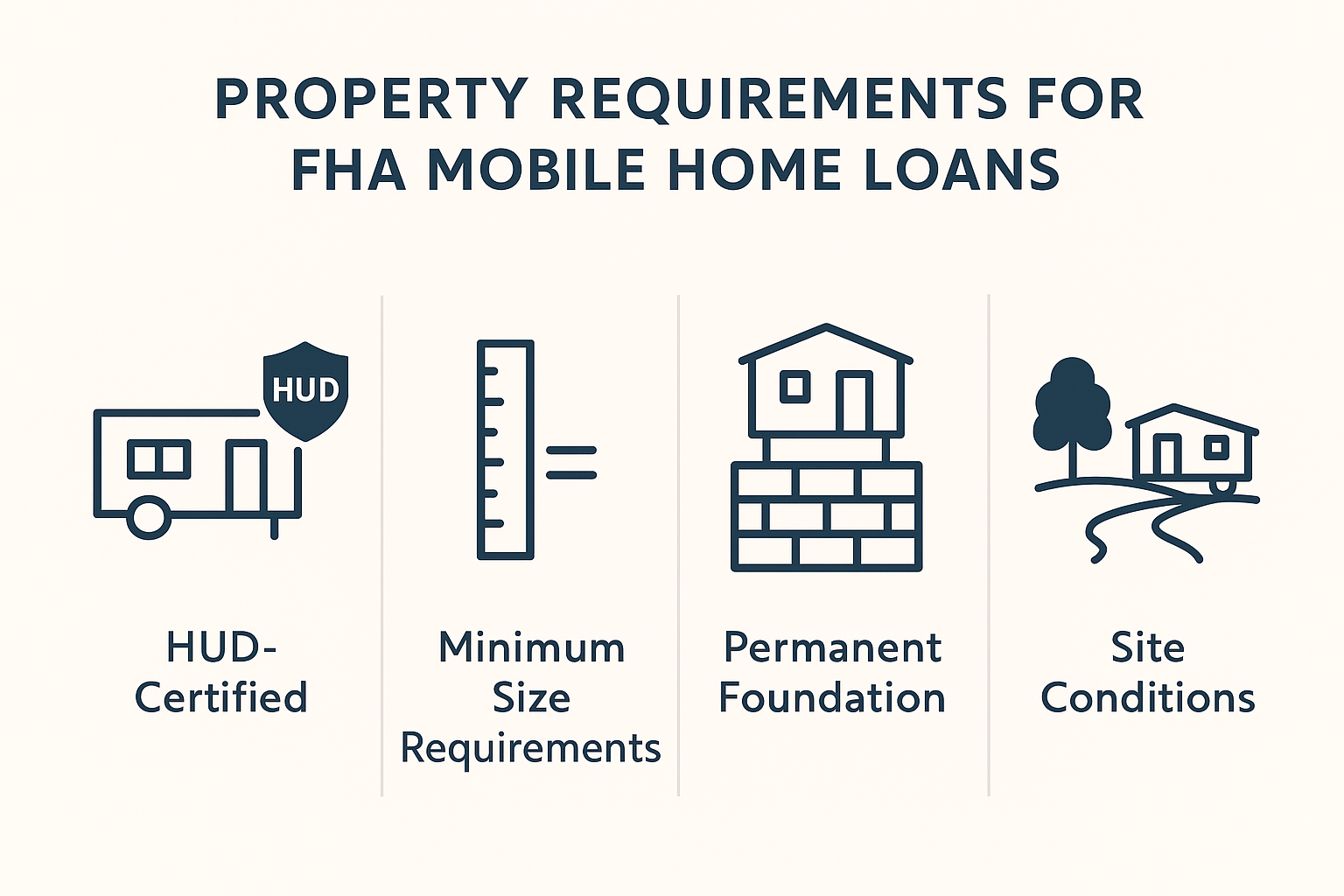

Property Requirements for FHA Mobile Home Loans

Not every mobile home qualifies for an FHA loan, even if you meet the credit and income requirements. The home itself has to meet certain standards, especially when it comes to safety, structure, and how it's installed. Here's what you need to know before moving forward.

The Home Must Be HUD-Certified

This is non-negotiable. FHA will only back loans for manufactured homes that meet HUD building standards, which means:

-

It was built on or after June 15, 1976

-

It has a red HUD certification label (metal plate) on the outside of each section

-

It comes with a HUD Data Plate (usually found inside a cabinet or closet)

If it’s missing either of these, the home likely won’t qualify, no matter how well it’s maintained.

Minimum Size Requirements

While the FHA doesn’t set an exact square footage in every case, the general rule is that the home must be:

-

At least 400 square feet (some lenders look for 600+)

-

Designed for single-family residential use

Tiny homes or RVs don’t make the cut, even if they’re on permanent land.

Foundation Requirements (Title II Only)

If you're applying for a Title II loan, the mobile home must be permanently attached to a foundation that meets FHA guidelines. That means:

-

The foundation has to be engineered and inspected to comply with HUD standards

-

The home must be tied down properly and capable of withstanding wind, snow, and other weather loads

-

It can’t be easily moved once installed

No skirting-only setups or mobile homes sitting on blocks. This is what separates real estate from personal property in the eyes of the FHA.

Site Conditions Matter Too

FHA wants to make sure the home is livable, not just technically up to code. The land it sits on must have:

-

All-weather access (a driveway or road you can use year-round)

-

Proper water and sewage hookups (or approved well/septic systems)

-

Utility connections (electric, gas, etc.)

If the site is off-grid or in an area with limited access to basic infrastructure, that may raise red flags during the appraisal process.

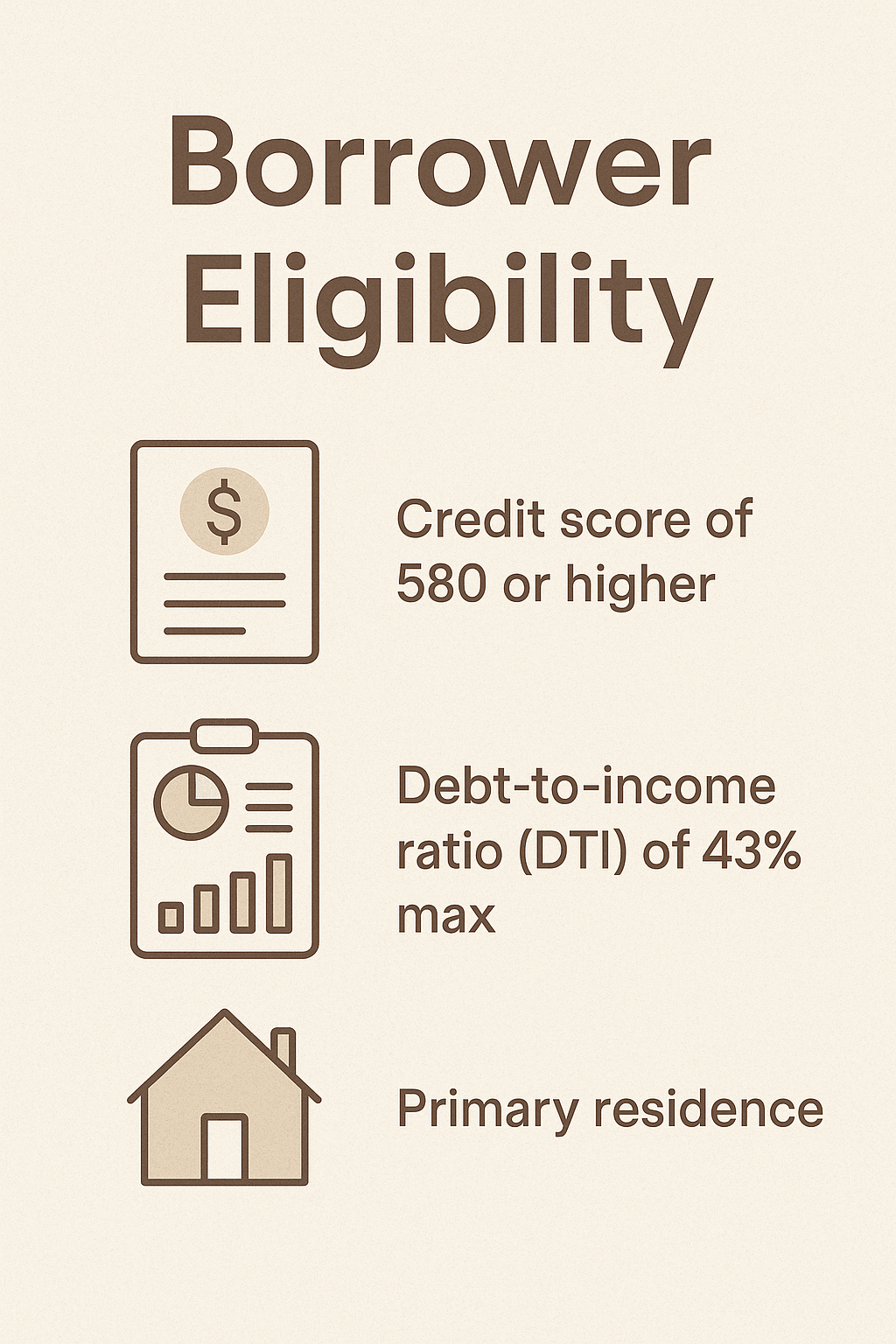

Borrower Eligibility

FHA loans are known for being more accessible than conventional financing, but you still need to meet a few basic requirements.

First, credit score plays a big role. If your score is 580 or higher, you’ll only need a 3.5% down payment. If it falls between 500 and 579, you may still qualify, but you’ll need to put down at least 10%. Anything below 500 usually disqualifies you.

Next is your debt-to-income ratio (DTI), basically how much of your income goes toward monthly debt payments. Most lenders stick to a limit of 43%, though some will allow up to 50% if you have strong compensating factors like savings or a steady job history.

You’ll also need to prove that the mobile home will be your primary residence (FHA loans can’t be used for vacation homes or investment properties), and that you have stable income going back at least two years.

Finally, there’s a CAIVRS check; a federal database that flags anyone who’s defaulted on government-backed loans. If you’re on that list, you’ll need to clear it before applying.

Loan Limits & Terms

|

Loan Type |

Loan Limit |

Max Term |

Setup Required |

|

Title I (home) |

$105K (single) / $193K (multi) |

20 yrs |

No land ownership or permanent foundation |

|

Title I (combo) |

$149K / $237K (single / multi) |

25 yrs |

Can include leased land + foundation optional |

|

Title I (lot) |

$43K |

15 yrs |

Financing land only |

|

Title II |

$524K–$1.21M (up to $1.81M in exceptions) |

30 yrs |

Must own land + permanent foundation |

Cost Breakdown & Mortgage Insurance

FHA loans are popular for a reason, they offer flexible credit requirements and low down payments. But it’s important to understand the full cost picture before signing anything, especially when it comes to mortgage insurance. Unlike conventional loans, FHA loans require both upfront and ongoing mortgage insurance, which protects the lender, not the borrower, in case of default.

Upfront Mortgage Insurance Premium (UFMIP)

One of the first costs you’ll encounter with an FHA loan is the Upfront Mortgage Insurance Premium, or UFMIP. This is a one-time fee equal to 1.75% of your total loan amount. You can pay it at closing, but most borrowers choose to roll it into the loan so it doesn’t require out-of-pocket cash.

Let’s say you’re borrowing $100,000. Your UFMIP would be $1,750. If you roll it into the loan, you’d technically be financing $101,750 instead.

Annual Mortgage Insurance Premium (MIP)

In addition to the upfront premium, FHA loans also charge an annual mortgage insurance premium (MIP) that’s built into your monthly mortgage payment. This is where many buyers are caught off guard.

The MIP rate varies depending on your loan term, amount, and down payment but most fall somewhere between 0.15% and 0.75% per year. The cost is broken down into monthly installments and added to your regular payment.

For example, on a $100,000 loan with a 0.55% MIP, you’d pay about $46 per month in mortgage insurance. And unlike private mortgage insurance (PMI) on conventional loans, FHA MIP typically doesn’t fall off automatically. In most cases, it stays for the life of the loan unless you refinance into a conventional mortgage later on.

Additional Costs to Expect

Aside from mortgage insurance, there are a few other expenses to factor into your budget:

-

Appraisal and inspection fees, especially if you’re applying for a Title II loan that requires a certified foundation

-

Loan origination fees and closing costs, which vary by lender

-

Dealer and title fees if you’re buying the mobile home through a retailer or third party

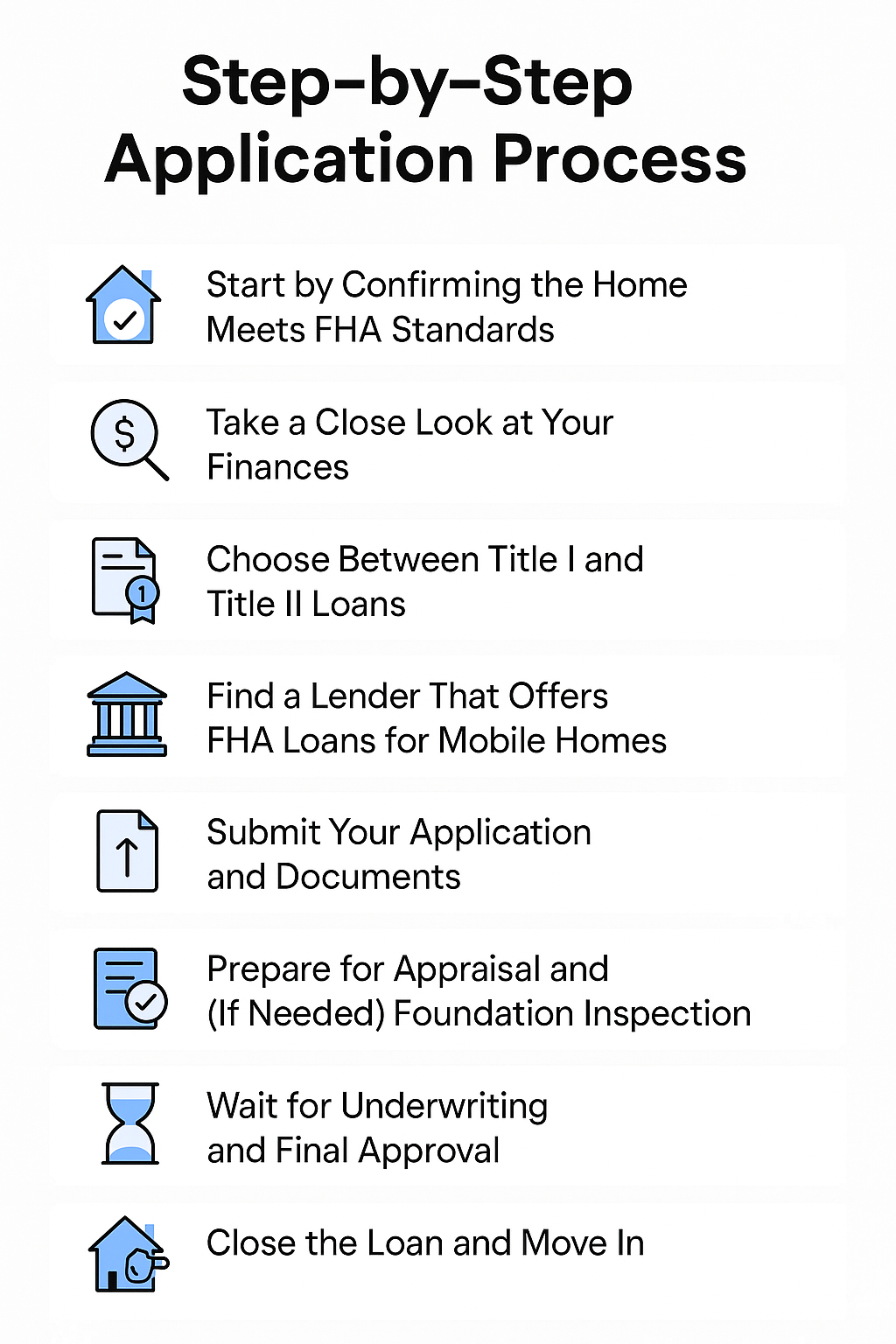

Step-by-Step Application Process

Applying for an FHA loan on a mobile home isn’t as complicated as it might seem but there are a few extra steps compared to a traditional home loan. Here's how the process typically goes, from start to finish:

1. Start by Confirming the Home Meets FHA Standards

Before you dive into paperwork, make sure the mobile home you’re planning to buy qualifies for FHA financing. The home must have been built after June 15, 1976, and display a HUD certification label. If you’re going for a Title II loan, the property also needs to be permanently attached to a foundation and classified as real estate.

If you’re buying a used home, ask for proof of HUD compliance and verify whether the foundation meets FHA guidelines. Skipping this step can cost you time and possibly your loan approval.

2. Take a Close Look at Your Finances

Next, review your financial standing. FHA loans are known for being flexible, but you’ll still need to meet some basic criteria. Most lenders want to see a credit score of at least 580 for a 3.5% down payment. If your score falls between 500 and 579, you may still qualify, but expect to put down at least 10%.

You’ll also need to show that you have steady income and a manageable debt load. In most cases, your total monthly debt payments shouldn’t exceed 43–50% of your gross income. Lenders will also run a CAIVRS check to make sure you don’t have any federal debts in default.

3. Choose Between Title I and Title II Loans

This is a crucial step. Title I loans are typically used when the home will be placed on leased land, such as in a mobile home park. Title II loans, on the other hand, require the home to be permanently installed on land you own or are buying at the same time.

Each option comes with its own loan limits, property requirements, and terms, so it’s important to choose the one that fits your setup.

4. Find a Lender That Offers FHA Loans for Mobile Homes

Not all FHA-approved lenders offer mobile home financing, especially for Title I loans. You can use HUD’s online search tool to find participating lenders, or ask your mobile home dealer for recommendations. It’s worth contacting a few to compare rates, fees, and experience with manufactured home financing.

5. Submit Your Application and Documents

Once you’ve chosen a lender, you’ll begin the formal application process. Be ready to provide:

-

Pay stubs or proof of income

-

Tax returns and bank statements

-

Government-issued ID

-

Details about the home and land (purchase contract, lease agreement, title documents)

This stage can move fairly quickly if you’ve prepared everything in advance.

6. Prepare for Appraisal and (If Needed) Foundation Inspection

After your application is in, the lender will schedule an FHA-approved appraisal to confirm the home’s value and basic condition. If you’re applying for a Title II loan, a certified engineer may also need to inspect the foundation to ensure it meets HUD guidelines.

These steps are important not just for loan approval, but to make sure your investment is sound.

7. Wait for Underwriting and Final Approval

During underwriting, the lender will carefully review all your documents, check your credit, verify employment, and assess the property’s eligibility. They may ask for additional paperwork or clarifications. If everything checks out, you’ll receive final loan approval.

8. Close the Loan and Move In

Once approved, you’ll head to closing, where you’ll sign the final loan documents, pay any remaining fees, and officially become a homeowner. If the loan covers both the home and land, the lender will coordinate with the dealer and title company to finalize everything.

Title I vs Title II: Which Fits?

One of the most important decisions you’ll make when applying for an FHA loan for a mobile home is whether to go with Title I or Title II financing. Both are backed by the FHA, but they’re built for different situations and choosing the right one can make a big difference in your approval odds, monthly payment, and loan flexibility.

When Title I Makes Sense

Go with Title I if you don’t own the land where your mobile home will be placed. This program allows you to finance just the home itself, just the lot, or both, making it a good fit for people leasing a lot in a mobile home park. It’s also useful if you’re financing the land and home separately.

Since the home doesn’t need to be permanently installed or classified as real estate, the application process is a bit more flexible. That said, loan amounts are lower and terms are shorter.

When Title II Is the Better Option

Title II is more like a traditional mortgage. It’s designed for mobile homes that are permanently affixed to land that you own or are buying as part of the loan. The home must meet stricter requirements, including a foundation inspection and real property classification, but the loan limits are much higher, and repayment terms are typically longer.

If you’re looking for the lowest possible monthly payment and plan to stay long term, this is usually the better route.

Title I vs Title II: Pros & Cons

|

Feature |

Title I |

Title II |

|

Land Ownership |

Not required (leased land allowed) |

Required (must own or buy land) |

|

Home Foundation |

Permanent foundation not required |

Must be permanently affixed to HUD-approved foundation |

|

Loan Term |

Up to 20–25 years (depending on use) |

Up to 30 years |

|

Loan Limits |

Lower (up to ~$237K for multi-section + lot) |

Higher (based on FHA county loan limits) |

|

Property Classification |

Personal property allowed |

Must be real property |

|

Flexibility |

More flexible for mobile parks or leased land setups |

Better for long-term ownership and stability |

|

Application Process |

Fewer property requirements |

Requires appraisal + foundation inspection |

Alternatives to FHA Loans for Mobile Homes

If you don’t qualify for a Title I or Title II loan, there are still other financing options worth exploring.

Chattel Mortgages are often used for mobile homes placed on leased land. They’re easier to get but come with higher interest rates, shorter terms, and fewer borrower protections.

You can also look into conventional manufactured home loans from Fannie Mae (MH Advantage) or Freddie Mac (Home Possible), which offer competitive rates if you meet stricter credit and income requirements.

Lastly, some buyers may qualify for USDA loans, VA loans, or state/local housing assistance programs, especially in rural areas or for veterans.

Tips to Boost Your Approval Odds

Getting approved for an FHA loan on a mobile home isn’t just about meeting the minimum requirements, it's also about making your application as strong as possible. Here are a few smart moves that can increase your chances:

-

Improve your credit score and save for a larger down payment. Even a small bump in your credit can open the door to better terms or a smoother approval process.

-

Shop around for lenders, especially if you’re applying for a Title I loan. Not every lender offers them, and rates can vary more than you’d expect.

-

Have all property documents ready, especially foundation certifications or inspection reports if you're applying under Title II. This helps avoid delays during underwriting.

-

Work with your dealer, if applicable, they often know which lenders are mobile-home-friendly and can help coordinate paperwork, appraisals, and timing.

FAQs

1. Can FHA loan funds be used for appliances?

Only for built-in appliances like ovens or dishwashers that are permanently attached. Standalone appliances (like a fridge or washer/dryer) aren’t covered by the loan.

2. Can I have more than one FHA loan for a mobile home?

Yes, but only under specific conditions. FHA allows one Title I loan and one Title II loan per borrower, as long as each meets eligibility criteria and is for your primary residence.

3. What’s the minimum size requirement for a mobile home?

To qualify for FHA financing, the home must be at least 400 square feet and built after June 15, 1976, in compliance with HUD standards.