You can finance mobile and modular homes like any other home. The six best mobile home loan programs are discussed in this article. Financing a mobile home is not as complicated as some people think. Let's uncover the main steps of finding good lenders and choosing the best option for your family!

Financing a Mobile Home: Exploring Your Options

Mobile and modular homes are the best home values for people who are looking for the many benefits of homeownership on a property of their choice. Retirees and families alike will find a design that meets their objectives. The technology and quality are constantly improving. The affordability factor means that you can get the same features for far less cost, and the good news is you can finance mobile and modular homes just as you can any other home.

Read also: Difference Between Mobile, Manufactured, Park, and Modular Homes

The major improvements in mobile and modular homes over the past ten years enable buyers to qualify for financing terms similar to those available for site-built homes. You will find that more lenders are now working with buyers of mobile and modular homes. The range of lending programs is similar to that for site-built homes. This article discusses the financial requirements and the property conditions you will need to meet.

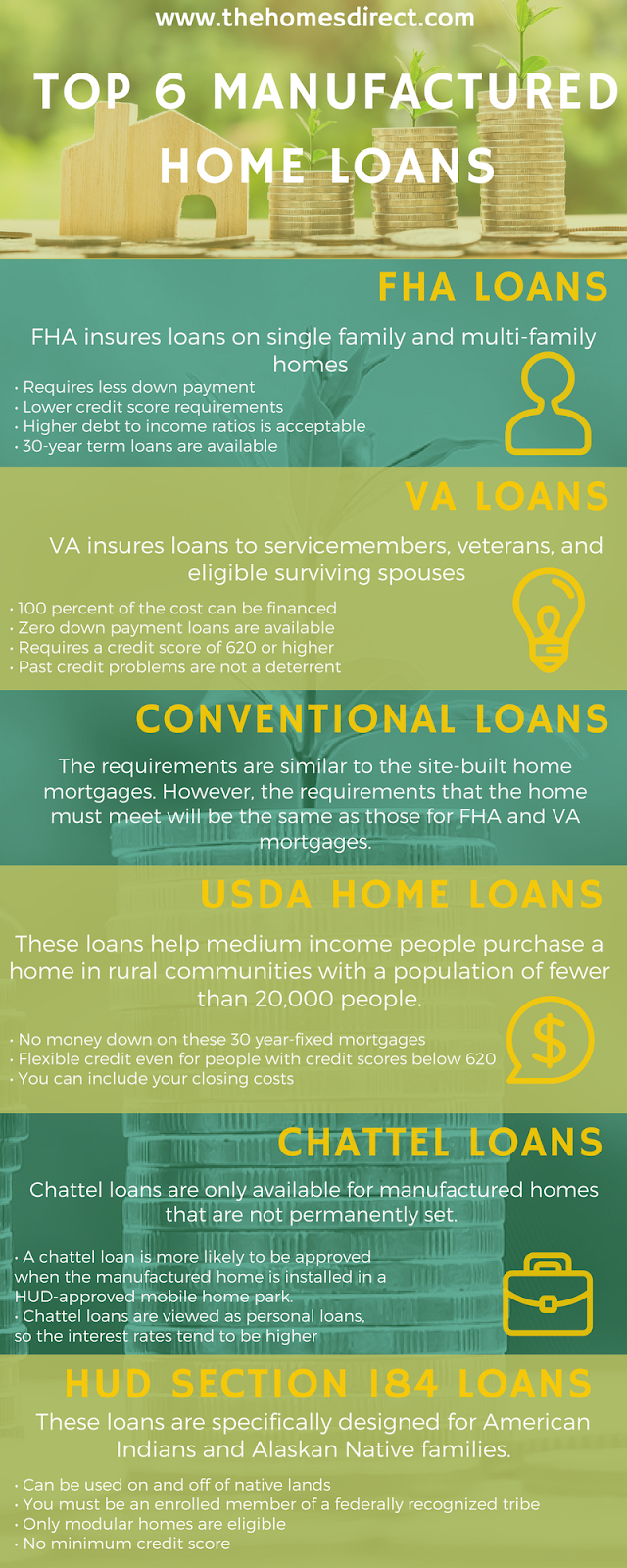

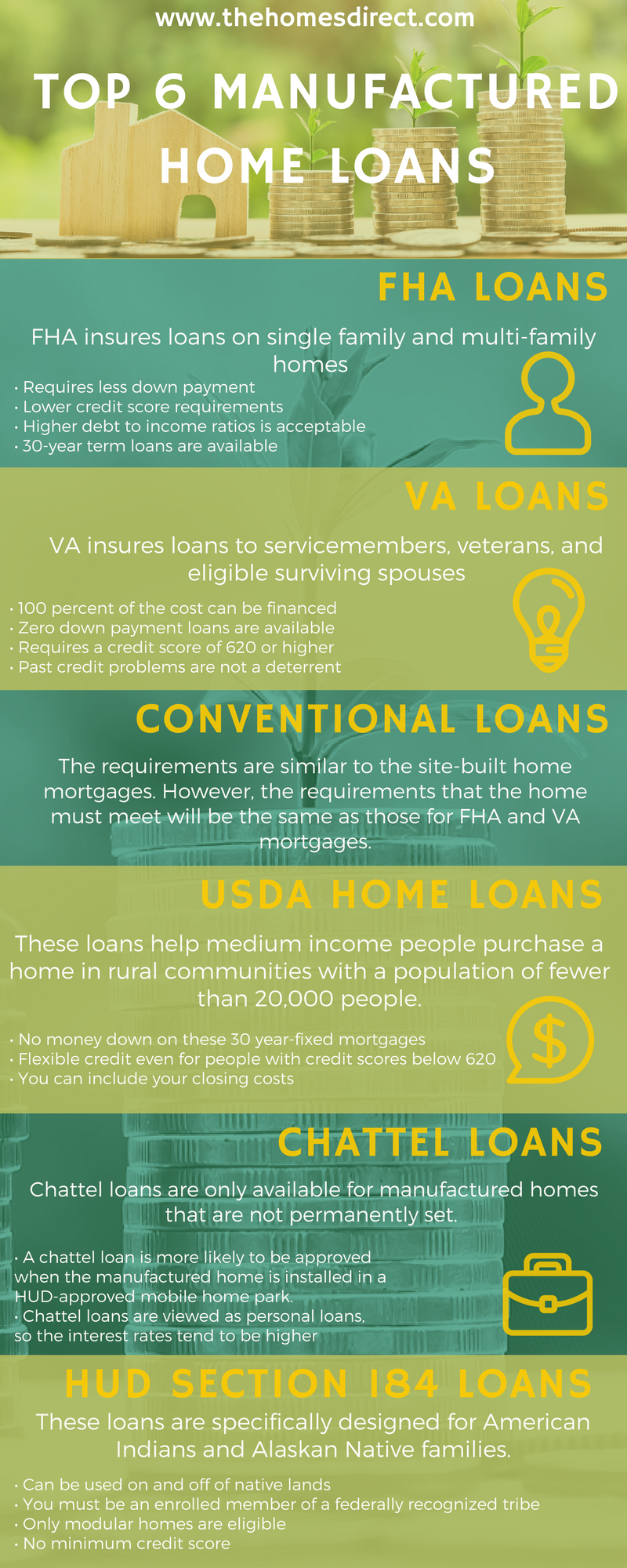

There are six types of loan programs available: FHA Loans, VA Loans, Conventional Loans, USDA Rural Development Loans, Chattel Loans, and HUD Section 184 Loans for Indians Buying a Modular Home. These are discussed below with some of the important qualifying criteria.

1. FHA Loans

-

Requires less down payment and often 3.5% will meet the down payment requirements.

-

Buyers with less than perfect credit are eligible.

-

Lower credit score requirements

-

Higher debt-to-income ratios is acceptable.

-

30-year term loans are available.

-

The home must be built after June 15, 1976.

-

The home must be permanently fixed to a foundation that meets FHA standards.

2. VA Loans

-

100 percent of the cost can be financed.

-

Zero down payment loans are available.

-

Requires a credit score of 620 or higher although buyers with a lower score may still be eligible.

-

Past credit problems are not a deterrent if the buyer can show an ability to repay the loan.

-

The other benefits and requirements of an FHA loan apply to VA loans.

3. Conventional Loans

These loans are available, and the requirements are similar to those for site-built home mortgages. However, the requirements that the home must meet will be the same as those for FHA and VA mortgages.

4. USDA Rural Development Loans

-

These loans are structured to help medium-income people purchase a home in rural communities with a population of fewer than 20,000 people.

-

No money down on these 30-year-fixed mortgages with low interest rates.

-

Flexible credit even for people with credit scores below 620.

-

You can include your closing costs.

5. Chattel Loans

-

Chattel loans are only available for mobile homes that are not permanently set. A mobile home can be installed on your property and not be permanently set.

-

A chattel loan is more likely to be approved when the mobile home is installed in a HUD-approved mobile home park.

-

A chattel loan may also be approved for installation on the applicant's property if the property meets FHA rules which require sufficient water availability and sewage disposal.

-

Financing a mobile home on land owned by the applicant will function the same way as financing an on-building.

-

Since chattel loans are viewed as personal loans, the interest rates tend to be higher.

6. HUD Section 184 Loans for Indians Buying a Modular Home

-

These loans are specifically designed for American Indians and Alaskan Native families.

-

It can be used on and off of native lands.

-

You must be an enrolled member of a federally recognized tribe.

-

Only modular homes are eligible.

-

No minimum credit score.

You can download the infographic here. You are free to share it online!

How Long Can You Finance a Mobile Home?

The length of financing a mobile home depends on the lender. However, you can expect to find loans of anywhere from five to 30 years, depending on the loan type.

The loans come with 30-year financing, and you may be able to secure them with a down payment as low as 3 percent. As an added benefit, interest rates on MH Advantage mortgages tend to be lower than those of most traditional loans for manufactured homes.

Considerations for Loan Repayment

Here are some specific considerations to pay attention to when you are financing a mobile home

-

Interest Rates and Terms

When compared to site-built homes, financing a mobile home

typically carries higher interest rates and shorter loan terms, especially when personal or chattel loans are utilized. An otherwise affordable housing payment may increase as a result of these expenses and timelines.

Knowing whether the mortgage you're getting is fixed-rate or adjustable-rate (ARM) is also crucial. Refinancing manufactured homes is challenging, so proceed with caution when using ARMs. -

Down Payments

Your credit score and the type of loan you apply for will determine how much you need for a down payment, but be prepared to put down at least 5% for the majority of loans (perhaps less for an FHA or VA loan).

Making a down payment with savings can be difficult. You can expedite the process by opening a distinct savings account for that reason and automatically funding it with each paycheck.

5 Steps for Financing a Mobile Home

Let’s get you all started on some quick tips and steps for financing a mobile home. What journey awaits you and how can you be prepared at your best? Read on

1. Determine your budget

Setting up a clear budget and figuring out how much you can afford for a home purchase are important steps before looking into your financing options. Make sure you can afford the monthly payments on your mobile home loan by considering factors like your income, savings, and monthly expenses.

2. Research lenders and loan options

Before financing a mobile home, it is crucial to do your homework on lenders and loan options in order to choose a reliable lender, get the best loan type, and negotiate favorable terms and interest rates. This ultimately results in savings and a more seamless financing experience by assisting you in meeting eligibility requirements, cutting expenses, and making sure the loan suits your budget.

Read also: 18 Typical Mobile Home Financing Terms You Have to Know

3. Compare interest rates and loan terms

As mentioned above, it is crucial to compare some lenders and find the best possible option for your family when financing a mobile home. Mortgage rates on mobile homes depend on how much you put down as collateral, your home loan terms, and your FICO score. Mortgage rates can be anywhere from 4% and 24%.

Find more detailed information: Financing Your Manufactured Home in 10 Easy Steps

4. Gather documentation

You will need to submit several documents to the lender to apply for financing a mobile home loan. These could consist of identification, bank statements, proof of income, and details about the mobile home you plan to buy. Having these files at hand can make the loan application process go more smoothly.

5. Submit your loan application and await approval

Upon selecting a lender and gathering the required paperwork, it's time to send in your loan application. Fill out the application completely and accurately; any errors or missing information could cause the approval process to drag on.

Following the submission of your loan application, the lender will examine your data and reach a determination. If accepted, you'll sign the required paperwork to complete the loan agreement and move on to the closing phase. Recall that even though getting financing for a mobile home may be difficult, there are still appropriate loan options available. You can obtain the financing required to make your purchase of a mobile home a reality by being aware of the procedure, investigating lenders, and carefully weighing your options.

What is the oldest mobile home that can be financed?

True mobile homes were built before June 15, 1976; homes built after that date are considered manufactured homes. Most lenders will only underwrite mortgages for true mobile homes if they conform to the current HUD standards for manufacturing and safety. However, you may be able to finance a mobile home built before June 15, 1976, with a different type of loan, like a personal loan or a chattel loan.

What is the lowest down payment for a mobile home?

The lowest down payment for a mobile home comes with FHA and VA loans, which can be as low as 3.5% or 0% respectively.

Are mobile home and modular house loans different?

While both mobile homes and modular houses offer factory-built housing solutions, the differences in their construction, foundation, and classification significantly impact the financing options available. Modular homes, due to their permanence and similarity to traditional homes, typically enjoy better financing terms and greater appreciation potential compared to mobile homes.

{kind=link}